Running a company today requires more than a good product; it requires a digital-first financial strategy. To find the most competitive small business loan rates 2026 has available, you need to understand how artificial intelligence and federal regulations have changed the game.

Whether you are looking for a long-term government-backed loan or a fast business line of credit, this guide covers the “new rules” of the financial landscape.

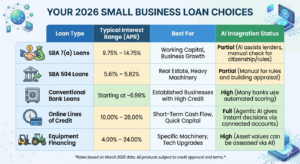

1. Current Small Business Loan Rates (March 2026)

Interest rates are the “price” of borrowing. Following the Federal Reserve’s late 2025 adjustments, the WSJ Prime Rate sits at 6.75%. Here is how that translates to your options:

| Loan Type | Typical APR / Interest Range | Best For | AI Integration |

| SBA 7(a) Loans | 9.75% – 14.75% | Working capital & growth | Partial |

| SBA 504 Loans | 5.61% – 5.82% | Real estate & equipment | Partial |

| Bank Loans | Starting at ~6.99% | High-credit businesses | High |

| Business Line of Credit | 10.00% – 28.00% | Short-term cash flow | Full |

| Equipment Finance | 4.00% – 24.00% | Machinery or tech | High |

2. Critical SBA Loan Requirements 2026

As of March 1, 2026, the Small Business Administration (SBA) implemented major updates. If you are pursuing an SBA loan, you must meet these new standards:

- 100% Citizenship Rule: A massive shift now requires 100% of owners to be U.S. citizens or nationals. Lawful Permanent Residents (green card holders) are no longer eligible for SBA 7(a) or 504 loans.

- No More SBSS Scores: For loans under $350,000, the SBA now lets lenders use their own credit analysis instead of the old FICO SBSS score.

- Manufacturing Perks: To boost local production, the SBA is waiving upfront fees (0%) for manufacturers on 7(a) loans up to $950,000 through September 2026.

3. The Rise of AI-Driven Approvals

The biggest trend this year is Agentic AI. Platforms like Bluevine and LendingClub now process a business line of credit in minutes by connecting directly to your accounting software.

- Real-Time Data: AI analyzes your live QuickBooks or Xero feed rather than looking at old tax returns.

- Predictive Health: Dashboards now send “loan readiness” alerts, so you apply when your cash flow is strongest.

- Biometric Security: Systems now use “behavioral biometrics” (like your typing patterns) to prevent identity theft during your application.

4. How to Qualify: The Four Pillars

To secure the best small business loan rates 2026 offers, focus on these benchmarks:

- Credit Profile: A personal score of 650+ is the standard for competitive rates.

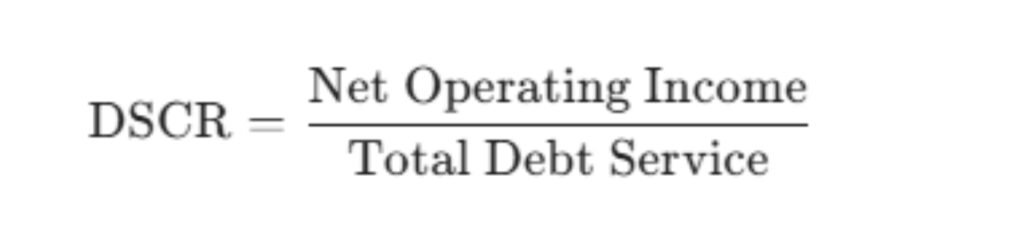

- Debt-to-Income (DTI): Lenders want a Debt Service Coverage Ratio (DSCR) of 1.25 or higher.

- Digital Readiness: Integrated accounting is no longer optional. “Disconnected” businesses face higher rates.

- Operational Stability: Most lenders look for 2+ years in business and $10k+ in monthly revenue.

5. Entrepreneur’s Resource List

- Books: “The Psychology of Money” by Morgan Housel & “Profit First” by Mike Michalowicz.

- Accounting: QuickBooks Online or Xero (with JAX AI assistant).

- Credit Tools: Nav Prime (monitoring) or Bloom+ (building credit via utilities).

- Forecasting: Float or Agicap for AI-powered cash flow visuals.

📘 Glossary of Essential Terms

- APR: The total annual cost of the loan, including interest and fees.

- Lien: A legal claim a lender has on your assets until the loan is paid.

- WSJ Prime Rate: The base rate banks charge their best customers (currently 6.75%).

❓ Frequently Asked Questions (FAQ)

1. Can Green Card holders get an SBA loan? Not under the SBA loan requirements 2026 update; 100% U.S. citizenship is now mandatory.

2. How fast can I get a business line of credit? With AI-driven fintechs, you can often see funds in 24 hours.

3. What is the best loan for buying a building? The SBA 504 loan offers the lowest rates (approx. 5.6%) for real estate.

What is Your Next Step? 2026 Small Business Loan Request Letter Template

If you need the lowest rates, use the SBA Lender Match Tool. If you need speed, explore a digital business line of credit. This template is designed to satisfy both the traditional review process and the “Real-Time Cash Flow” requirements of 2026 AI underwriting systems. Use this as a cover letter for your application.

To get started, you can use this template as a cover letter for your application.

[Your Name / Business Name]

[Business Address]

[Phone Number]

[Email Address]

[Date]

To: [Loan Officer Name or “Underwriting Department”] [Lender Name (Bank or Fintech)] [Lender Address]

Subject: Loan Request – $[Requested Amount] for [Business Name]

Dear [Loan Officer Name or “Lending Team”],

I am writing to formally request a [Type of Loan, e.g., SBA 7(a) or Fintech Line of Credit] in the amount of $[Amount] for my business, [Business Name]. Our company has been in operation for [Number] years, specializing in [Brief Industry Description].

1. Purpose of Funding We intend to use these funds to [Specific Purpose, e.g., purchase high-efficiency manufacturing equipment / expand our digital marketing reach]. This investment is projected to increase our monthly revenue by [X]% within the next [Number] months by [Briefly explain how, e.g., increasing production capacity].

2. Financial Health & 2026 Compliance * Citizenship: In accordance with the March 2026 SBA guidelines, I confirm that 100% of the ownership of [Business Name] consists of U.S. citizens/nationals.

- Credit & Stability: Our business maintains a personal credit score of [Your Score] and has seen consistent monthly revenue of $[Average Revenue] over the last 12 months.

- Digital Integration: We have already integrated our [QuickBooks/Xero] accounts with our banking portal to allow for the real-time cash flow analysis required for modern underwriting.

3. Repayment Strategy Based on our current cash flow and a projected Debt Service Coverage Ratio (DSCR) of [Your Ratio, e.g., 1.45], we propose a repayment term of [Number] months. We plan to automate these payments via ACH to ensure timely delivery and maintain our strong credit standing.

4. Supporting Documents Attached to this letter, please find:

- Three years of business and personal tax returns.

- Current Balance Sheet and YTD Profit & Loss Statement.

- A detailed itemized list of the equipment/services to be purchased.

- [Optional: Business Plan / Market Analysis].

Thank you for your time and for considering [Business Name] as a partner in your lending portfolio. I am available at your convenience to discuss this application further or provide additional digital access to our financial data.

Sincerely,

[Your Signature]

[Your Printed Name]

[Your Title]