In 2026, the financial world looks different than it did a decade ago. We’ve seen the rapid integration of AI, the cooling of post-pandemic inflation, and a “new normal” for interest rates. But according to Christopher Tan, a CEO who manages $1.7 billion in assets, the most important financial lessons for 2026 aren’t about complex algorithms—they are about the human heart.

If you want to know what to do with your money this year, it’s time to look past the spreadsheets and focus on sufficiency, simplicity, and the “Three Cs.”

Table of Contents

1. The Core Philosophy: “Rich” vs. “Looking Rich”

The biggest financial trap in 2026 is the trap of comparison. Christopher Tan notes that many successful professionals feel financially insecure not because they lack money, but because they are constantly comparing their lifestyle to their peers.

- The “Luxury Trap”: There is a dangerous cycle in wealth management: “Luxury once enjoyed becomes a necessity.” When you upgrade to a condo or a luxury car, that becomes your new baseline. You end up working “your butt off” just to pay a mortgage for a home you’re too busy to enjoy.

- The 2026 Reset: Instead of chasing more, aim for Simplicity. As Tan puts it, “Simplicity once appreciated becomes a sanctuary.” True financial freedom is having a life that doesn’t require you to make “wrong decisions” just to keep up with your debt.

2. The “Three Cs” Strategy for 2026

If you aren’t an expert investor or you find market volatility stressful, Tan suggests focusing on these three pillars:

- Cash Flow Management: Spend below your means and keep a healthy surplus. In 2026, use low-risk instruments like Treasury bills for your “rainy day” funds.

- Coverage Management: Buy the insurance you need, but pay as little as possible. Avoid complex products that over-insure you unnecessarily.

- Retirement Account Management: Maximize government-backed accounts (like CPF in Singapore). With guaranteed returns of 4% to 6%, these are the best risk-free investments available.

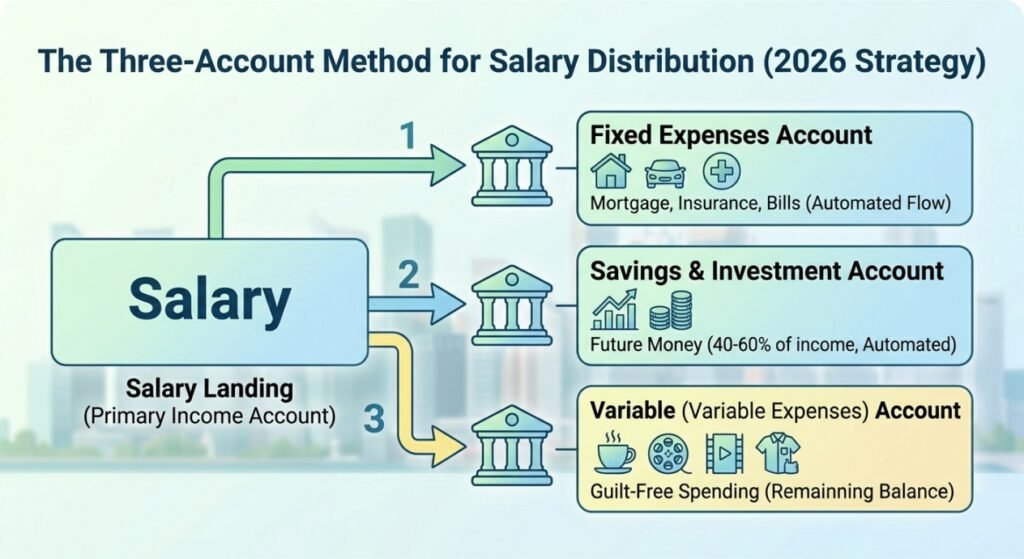

3. How to Handle Your Salary: The Three-Account Method

Managing money in 2026 should be automated. When your paycheck hits your bank, follow this simple flow:

- Income Account: Where your salary lands.

- Fixed Expenses Account: Set up a standing instruction to move money here for your mortgage, insurance, and bills.

- Savings/Investment Account: Move your “future money” here immediately.

- The “Guilt-Free” Spend: Whatever is left in your Income Account is yours to spend.

4. Investing in Your “Ikigai”

Money is just a tool to enable your life. In 2026, stop spending to impress people you don’t even like. Instead, allocate your funds to:

- Experiences over Objects: Spending on memories (like a 30th-anniversary dinner) brings immeasurable joy compared to physical goods.

- Health as an Investment: Health requires “compounding” time, just like money. Don’t sting on comprehensive screenings.

- Education and Skills: In the age of AI, your ability to provide human value is your greatest asset.

5. Teaching the Next Generation

Build character in your children by teaching them the difference between Needs and Wants. Encourage them to pay for their own “wants” through part-time work and implement the “Giving Rule”—teaching them to give a portion of their first paycheck back to their parents as an act of gratitude.

Identity vs. Net Worth

Your identity is not your net worth. Whether you are driving a 9-year-old car or a brand-new Maserati, your security must come from within. In 2026, the smartest thing you can do with your money is to build a life of sufficiency, not a life of show.

Disclaimer: befinanciallyfree.net/ provides educational content on wealth protection. This article is for informational purposes only and does not constitute legal, medical or financial advice. Always consult with a licensed professional regarding your specific situation.