Imagine waking up on a Tuesday morning, not to the jarring ring of an alarm clock set for a commute, but to the natural light filtering through your window. You check your phone—not for urgent “ASAP” emails from a boss, but to see how your automated income streams performed overnight. You have enough in the bank to cover your life for the next thirty years, regardless of whether you ever “work” another hour.

Table of Contents

This is the reality of Financial Freedom in 2026

For decades, the path to wealth was predictable: graduate, find a stable 9-to-5, climb the corporate ladder, and hope the 401(k) math worked out by age 65. But the “Old Rules” have evaporated. In a world defined by generative AI, shifting interest rates, and the total decoupling of “work” from “location,” the roadmap to independence has been completely rewritten.

The New Financial Frontier

We are living through the most significant shift in wealth creation since the Industrial Revolution. Financial freedom in 2026 isn’t just about a “number” in a brokerage account; it’s about Time Sovereignty. It’s the ability to leverage technology to buy back your hours.

Whether you are aiming for Fat FIRE (retiring with a high-consumption lifestyle), Coast FIRE (investing early so you only work for “fun” money), or simply escaping the paycheck-to-paycheck cycle, the strategy remains the same: Building a Fortress of Stability and an Engine of Growth.

Why Traditional Advice Fails Today

If you’re still following 2010-era advice, you’re falling behind. Inflation has changed the “Safe Withdrawal Rate,” and AI has disrupted the traditional “stable career.” To be financially free today, you must be more than a saver; you must be an architect of your own economy.

In this guide, we aren’t just going to talk about “cutting back on lattes.” We are going to dive into:

- The 2026 Fortress: Protecting your wealth against digital volatility.

- The AI Multiplier: How to turn “side hustles” into automated equity.

- The Psychology of the Gap: Why happiness actually lives in the space between your expectations and your reality.

The door to independence is wider than ever, but the locks have changed. This is your key.

Phase 1: The Fortress (Defense & Stability)

Before you can build an engine of growth, you must build a wall of protection. In the 2026 economy, “stability” is defined by three specific pillars: Cash Flow Engineering, Strategic Debt Exit, and Modern Protection.

1. Cash Flow Engineering: High-Yield Liquidity

In 2026, keeping your emergency fund in a standard “big bank” checking account is effectively losing money every day.

- The 5% Benchmark: Aim for High-Yield Savings Accounts (HYSA) or Money Market Funds that yield at least 5% APY.

- The “3-6-12” Rule: In the AI-driven job market, the old “3-month emergency fund” is risky. Aim for 3 months of bare essentials in cash, 6 months in a liquid HYSA, and 12 months of “buffer” in low-risk Treasury Bills (T-Bills) or short-term bonds.

2. The Strategic Debt Exit

Not all debt is created equal. To be financially free, you must categorize your debt by its “toxicity.”

- Toxic Debt (15%+ APR): Credit cards and high-interest personal loans. These are “wealth-killers.” Use the Debt Avalanche method (paying the highest interest first) to kill these immediately.

- Management Debt (4%–7% APR): Modern mortgages or student loans. In 2026, if your savings account pays 5% and your mortgage is 4%, there is a mathematical argument for not paying it off early.

- The “Refi” Trigger: Set automated alerts for when mortgage or student loan interest rates drop by more than 0.75%. This is your signal to refinance and lower your monthly overhead instantly.

3. Modern Protection: Beyond Life Insurance

Your greatest asset in 2026 is your ability to earn. If that is compromised, the fortress crumbles.

- Income Protection (Disability): Most people insure their cars but not their paychecks. Ensure you have “Own-Occupation” disability insurance.

- Cyber-Liability: As a digital-first earner, a hacked account or identity theft can freeze your assets. 2026-era protection plans now include AI-fraud monitoring and legal recovery funds.

- The “Health-Wealth” Link: High-Deductible Health Plans (HDHP) paired with a Health Savings Account (HSA) remain the ultimate “triple-tax-advantaged” fortress tool.

The Goal: By the end of Phase 1, you should be able to lose your primary income source today and live exactly the same lifestyle for at least 6 months without touching your long-term investments.

Phase 2: The Engine (Wealth Building & The AI Multiplier)

If the Fortress is your defense, the Engine is your offense. To achieve true financial independence in the mid-2020s, you must move beyond “saving” and start architecting equity.

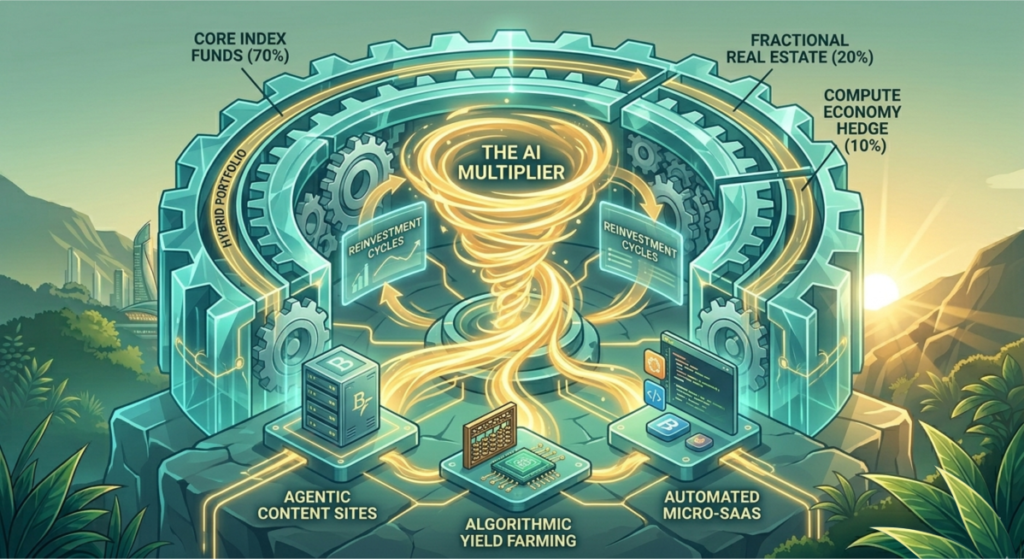

1. The 2026 “Hybrid” Portfolio

The old 60/40 stock-to-bond ratio has been replaced by a more dynamic model that accounts for digital assets and fractional ownership.

- The Core (70%): Low-cost, total-market index funds (like VTI or VOO). These remain the most reliable long-term wealth creators.

- The Satellite (20%): Real Estate and Alternative Assets. Use Fractional Investing platforms to own pieces of institutional-grade rental properties or private equity with as little as $500.

- The Tech Hedge (10%): A dedicated allocation to the “Compute Economy”—companies building the infrastructure for AI, robotics, and decentralized finance (DeFi).

2. Using AI to Scale Passive Income

The biggest shift in 2026 is the ability for a single individual to operate with the power of a ten-person agency. This is where you create “Passive Income 2.0.”

- Agentic Content Streams: Use AI agents to manage “faceless” niche websites or YouTube channels. By automating research, SEO, and initial drafting, you can maintain a portfolio of revenue-generating sites (like befinanciallyfree.net/) with only a few hours of oversight per week.

- Algorithmic Yield Farming: For the tech-savvy, AI-driven bots can now manage “yield farming” in stablecoin pools, automatically moving liquidity to the highest-paying, lowest-risk protocols to maximize interest.

- Automated SaaS (Software as a Service): Micro-SaaS tools built with AI-assisted coding can solve specific financial problems (like a specialized “Fire Calculator for Freelancers”) and generate recurring monthly subscription revenue.

3. The Power of “Compounding Efficiency.”

In the past, compounding only applied to your money. In 2026, it applies to your systems.

- The Rule of Automation: Every financial task that takes you more than 15 minutes a week (budgeting, rebalancing, bill pay) should be outsourced to an AI tool.

- Reinvestment Cycles: Instead of spending your AI-generated side income, funnel 100% of it back into your “Core” index funds. This creates a “double-compounding” effect where your work builds assets, and those assets build more wealth.

4. Avoiding the “Shiny Object” Trap

With so many AI tools available, the biggest risk in 2026 is complexity.

- The 80/20 Rule: 80% of your wealth will still come from 20% of your actions—specifically, consistent monthly investing. AI should be used to support your engine, not to turn your financial life into a high-risk laboratory.

The Engine Goal: By the end of Phase 2, your “passive” income (investments + AI streams) should cover at least 50% of your basic living expenses. At this point, you aren’t just working for a paycheck—you’re working for “bonus” wealth.

Phase 3: The Lifestyle (The 2026 FIRE Blueprint)

Financial independence in the mid-2020s is about designing your days, not just escaping a job. With the rise of the “borderless professional,” your location and your spending habits are your two biggest levers for freedom.

1. Choosing Your FIRE Path

Not everyone wants to live on rice and beans to retire early. In 2026, three distinct “FIRE” (Financial Independence, Retire Early) models have emerged as the gold standards:

- Coast FIRE (The Early Starter): You invest aggressively in your 20s or 30s until your “core” portfolio is large enough that, even without another cent invested, it will grow to your retirement goal by age 60.

- The Benefit: You can stop “hustling” and take a lower-paying, lower-stress job that simply covers your monthly bills.

- Lean FIRE (The Minimalist): You optimize your life for extreme efficiency, typically living on $30,000–$40,000 a year.

- The Benefit: You can “retire” much sooner because your “Number” is lower (usually around $1M).

- Fat FIRE (The Abundance Model): You build an engine capable of supporting a $150,000+ annual spend.

- The Benefit: No compromises on travel, luxury, or healthcare. This usually requires scaling an AI-driven business or reaching executive-level equity.

2. Geographic Arbitrage: The “Global Paycheck.”

One of the most powerful tools in 2026 is Geographic Arbitrage—earning in a strong currency (like USD or EUR) while living in a region with a significantly lower cost of living.

- The “Digital Nomad” 2.0: Countries like Portugal, Spain, and Malaysia have streamlined their “Digital Nomad Visas,” making it easier to maintain tax residency while living in paradise.

- Domestic Arbitrage: You don’t have to leave the country. Moving from a high-tax city (like New York or San Francisco) to a “low-cost, high-amenity” hub can effectively give you a 30%–40% raise overnight.

3. The 2026 Withdrawal Strategy

In a world of higher volatility, the old “4% Rule” has evolved. In 2026, experts suggest a Dynamic Spending Strategy:

- The Guardrails Method: If the market is up, you take your full withdrawal. If the market dips more than 10%, you reduce your “discretionary” spending by 15% for that year. This ensures your portfolio never hits a “point of no return.”

4. Health & Longevity: The Ultimate Expense

In 2026, healthcare remains the biggest “unknown” variable in the FIRE equation.

- HSA Optimization: Your Health Savings Account is your “Super IRA.” Use it for tax-free growth and save your receipts—you can reimburse yourself decades later, tax-free.

- Preventative Wealth: Investing in your physical health today (sleep, nutrition, fitness) is the best way to lower your “burn rate” in your 50s and 60s.

The Lifestyle Goal: By the end of Phase 3, you should have identified your “FIRE Number” and mapped out exactly where in the world that number allows you to live like royalty.

Phase 4: Psychological Wealth (The Mindset Gap)

Financial freedom is a hollow victory if you haven’t mastered your relationship with money. Many spend decades building a “Number,” only to realize they’ve forgotten how to live once they hit it.

1. Closing the Expectations Gap

Happiness in the 2020s isn’t found in a higher bank balance; it’s found in the formula: Happiness = Reality – Expectations. * The Hedonic Treadmill: As your income grows, your lifestyle naturally “creeps” upward. If you don’t intentionally cap your expectations, you will be a “Wealthy Prisoner”—someone with millions who still feels like they don’t have enough.

- The “Enough” Metric: Define your “Enough” before you reach it. Write down exactly what your ideal Tuesday looks like. If that Tuesday costs $5,000 a month, and you’re earning $10,000, you are winning. If you keep moving the goalpost to $15,000, you are losing.

2. The Arrival Fallacy

Many people believe that “once I hit X amount, all my stress will vanish.” This is the Arrival Fallacy.

- Internal vs. External: Money solves money problems (bills, debt, access). It does not solve human problems (loneliness, lack of purpose, health).

- Practicing Retirement: Don’t wait for your FIRE date to live your life. Use your “Fortress” to take mini-retirements or 4-week sabbaticals now. This tests whether you actually like the lifestyle you’re building toward.

3. Designing Your “Post-Work” Identity

When you stop working for a paycheck, you lose a major source of social identity and structured time.

- The Three Pillars of Purpose: To stay mentally sharp, you need Autonomy (control), Complexity (a challenge), and a Connection between effort and reward.

- Philanthropy and Giving: In 2026, the most satisfied “Retirees” are those who have shifted from Success to Significance. Whether it’s mentoring, local community projects, or global environmental initiatives, having a cause larger than your own portfolio is the secret to longevity.

4. The “Fear to Freedom” Shift

Transitioning from Saving (the mindset of Phase 1 & 2) to Spending (the mindset of Phase 3 & 4) is a massive psychological hurdle.

- Die with Zero: Consider the philosophy of “Die with Zero”—maximizing your life experiences while you have the health and energy to enjoy them, rather than hoarding wealth for a “someday” that may never come.

The Ultimate Goal: Financial freedom is the moment you stop asking “Can I afford this?” and start asking “Is this how I want to spend my limited time on Earth?”

Conclusion: Your 2026 Checklist

You now have the full blueprint for befinanciallyfree.net/.

To summarize:

- Build the Fortress: 5% APY liquidity and toxic debt elimination.

- Ignite the Engine: Hybrid portfolios and AI-leveraged side income.

- Choose the Lifestyle: Pick your FIRE path and leverage geographic arbitrage.

- Master the Mindset: Cap your expectations and find your purpose beyond the “Number.”

Disclaimer: befinanciallyfree.net/ provides educational content on wealth protection. This article is for informational purposes only and does not constitute legal, medical or financial advice. Always consult with a licensed professional regarding your specific situation.