Are you tired of watching your hard-earned money sit in a standard savings account, earning pennies while prices at the grocery store keep climbing? You aren’t alone. In our 2026 US Treasury Guide, we’re breaking down a shift that smart savers are making right now: moving cash from big banks into U.S. Treasury Bills (T-Bills).

For years, the “big banks” were the default home for extra cash. But as we move through 2026, the math has changed. Whether you are saving for a wedding, a house down payment, or just a rainy day, understanding the 2026 US Treasury Guide principles can help you earn significantly more interest with virtually zero extra risk.

Table of Contents

What Are T-Bills and Why Are They Winning?

Treasury Bills, or T-Bills, are short-term loans you give to the U.S. Government. In exchange, the government pays you interest. They are widely considered the safest investment on the planet because they are backed by the “full faith and credit” of the United States.

In 2026, T-Bills are outperforming traditional savings accounts for three main reasons:

- Higher Rates: While many big banks still offer measly rates on standard savings, T-Bills have stayed competitive with inflation.

- Tax Breaks: This is the “secret sauce.” The interest you earn on T-Bills is exempt from state and local income taxes. If you live in a high-tax state like California or New York, this makes your “real” take-home pay much higher than a bank account.

- Liquidity: You can buy T-Bills that mature in as little as 4 weeks. You aren’t locking your money away for years.

Key Feature: Top US Banks vs. 4-Week T-Bills (April 2026)

To give you a clear picture of this US Treasury Guide 2026, let’s look at how the 4-week T-Bill stacks up against the “Big Four” banks and top-tier high-yield savings accounts (HYSA).

| Financial Institution / Product | Current APY (Estimated) | State Tax Exempt? | Minimum Deposit |

| 4-Week U.S. T-Bill | 3.63% | Yes | $100 |

| High-Yield Savings (Online) | 4.00% – 4.21% | No | $0 – $100 |

| Chase (Standard Savings) | 0.01% | No | $0 |

| Bank of America (Standard) | 0.01% | No | $0 |

| Wells Fargo (Way2Save) | 0.01% | No | $25 |

Pro Tip: While some online High-Yield Savings Accounts (HYSAs) show a higher “headline” rate than T-Bills, remember to subtract your state income tax from the bank rate. Often, the T-Bill wins on a “net” basis!

How to Get Started: A Simple 3-Step Process

Following this 2026 US Treasury Guide doesn’t require a degree in finance. You can start with as little as $100.

1. Choose Your Platform

You can buy T-Bills directly from the government at TreasuryDirect.gov, or through most major brokerage accounts like Fidelity, Charles Schwab, or Vanguard. Brokerages are often easier to use because they have more modern websites.

2. Pick Your Maturity

For maximum flexibility, most people start with the 4-week or 8-week T-Bill. This ensures your money is never out of reach for too long.

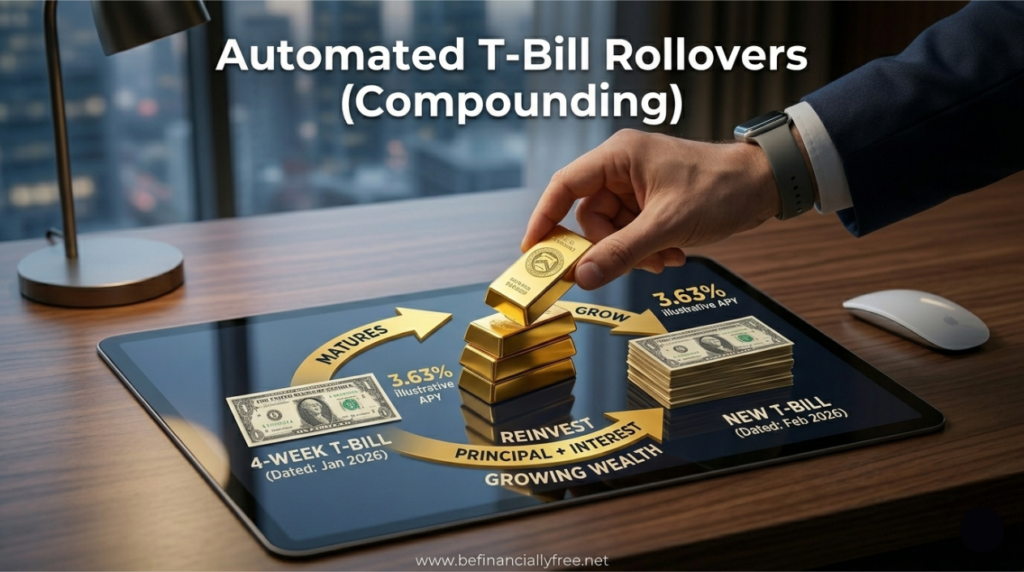

3. Set Up “Reinvestment”

If you don’t need the cash right away, you can tell the system to “roll over” your T-Bill. When one 4-week bill ends, it automatically buys a new one. This creates a “ladder” of income that hits your account every month.

Is There a Catch?

Nothing is perfect. The main “downside” to T-Bills compared to a savings account is that you can’t withdraw the money instantly via an ATM. If you buy a 4-week bill, your money is committed for those 28 days. For this reason, we recommend keeping your emergency fund (3-6 months of bills) in a liquid savings account and using T-Bills for your extra savings.

Final Thoughts for 2026

The goal of being financially free is to make your money work as hard as you do. By using this US Treasury Guide 2026, you’re cutting out the middleman (the bank) and going straight to the source. You get higher security, better tax treatment, and more money in your pocket.

Stop letting the big banks profit off your deposits. Take control of your cash today!

Disclaimer: befinanciallyfree.net/ provides educational content on wealth protection. This article is for informational purposes only and does not constitute legal, medical or financial advice. Always consult with a licensed professional regarding your specific situation.